Oil’s war premium has evaporated — but the US–Iran deal may have reset a higher floor for crude prices.

The US–Iran memorandum aimed at ending months of conflict across the Middle East has triggered a sharp repricing in global oil markets. Traders have rushed to unwind the geopolitical risk premium that had driven crude higher during the crisis, betting that the easing of tensions will restore disrupted supply and bring millions of barrels of Middle Eastern oil back into global flows.

But while the immediate threat of a supply shock has eased, energy analysts warn that investors may be overlooking a more fundamental reality: the agreement is only a framework for future negotiations, not a binding resolution.

Meanwhile, global oil inventories remain historically depleted, and even a sizeable supply surplus may not be enough to push crude back to pre-war levels.

Instead, analysts say the deal may have established a new, higher floor for oil prices.

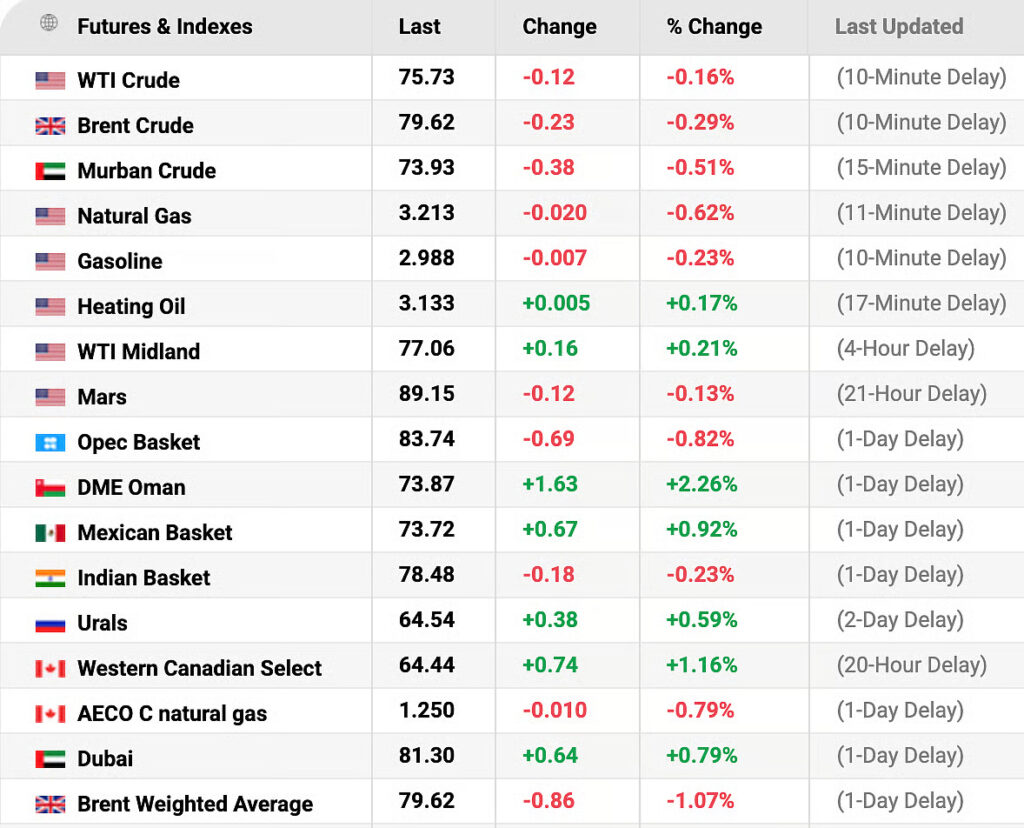

As of 11:24 a.m. Tokyo time on Friday (June 19), Brent hovered just below $80, while WTI slipped to $75.73 and Murban crude stood at $73.93.

Markets breathe a sigh of relief

Oil prices have fallen sharply since Washington and Tehran announced a 14-point Memorandum of Understanding aimed at ending hostilities and opening negotiations toward a broader settlement.

Brent crude slipped below $80 a barrel for the first time since March as markets priced in the reopening of the Strait of Hormuz — the world’s most important oil shipping corridor — and the gradual return of more than 13 million barrels per day of disrupted regional production.

For traders, the message appeared straightforward: lower geopolitical risk means more oil, and more oil means lower prices.

Yet the reality is considerably more complex.

MoU: not a peace treaty

Despite market optimism, the US–Iran agreement is not a comprehensive peace accord.

It is a memorandum establishing a framework for negotiations, with both governments agreeing to seek a final settlement within 60 days, subject to extension if talks continue to progress.

However, many of the issues that originally drove the conflict remain unresolved. These include:

- permanent sanctions relief for Iran

- the future of Iran’s nuclear programme

- long-term regional security arrangements

- mechanisms to enforce compliance

- and durable guarantees for freedom of navigation through the Strait of Hormuz

Even Iran’s commitment on maritime security falls short of a legally binding guarantee, instead pledging to use its “best efforts” to facilitate commercial shipping.

That distinction matters. If negotiations collapse or either side fails to comply with future commitments, the geopolitical risk premium currently unwinding in oil markets could quickly re-emerge.

Markets pricing in an oil surplus

Investors, however, appear more focused on the supply outlook.

The International Energy Agency (IEA), in its first long-term outlook for 2027, projects global oil demand to rise by roughly 2 million barrels per day, while production capacity could expand by as much as 8 million barrels per day.

That would leave the market with an apparent surplus approaching 5 million barrels per day.

Under normal circumstances, such an imbalance would exert sustained downward pressure on prices.

Expectations of abundant supply have become one of the key drivers behind the recent decline in Brent crude.

Why a glut may not produce cheap oil

History suggests supply is only one side of the equation.

During months of conflict, governments and commercial buyers drew heavily on oil inventories to offset disrupted production.

Global petroleum stockpiles have been depleted at an estimated rate of 3.8 million barrels per day, including around 2.4 million barrels of crude and 1.4 million barrels of refined products.

OECD emergency inventories have fallen to their lowest levels in more than three decades, while the U.S. Strategic Petroleum Reserve remains near multi-decade lows after years of emergency drawdowns.

Those depleted inventories effectively represent future demand.

Instead of immediately overwhelming the market, much of the additional oil expected from Iran and other Gulf producers may first be absorbed by governments rebuilding strategic reserves and refiners replenishing commercial storage.

In other words, incremental production gains may initially go toward refilling depleted inventories rather than expanding freely available market supply.

Production will not return overnight

Another factor limiting downside pressure is timing.

Although sanctions relief could eventually allow Iran to lift exports significantly, restoring full production capacity across the region will take time.

Oil fields require maintenance after prolonged disruptions, export infrastructure must be fully reactivated, and shipping schedules will need time to normalise.

Governments are also unlikely to flood the market immediately if doing so risks a sharp decline in prices.

Several major producers retain the flexibility to adjust output depending on market conditions.

A new equilibrium for oil

Analysts increasingly argue that the post-war oil market may settle into a very different configuration from the one that existed before the conflict.

According to Ole Hansen, Head of Commodity Strategy at Saxo Bank, depleted inventories, strategic reserve rebuilding, gradual production recovery and stronger seasonal demand are likely to support prices even if geopolitical tensions continue to ease.

Futures markets appear to support that view.

Brent crude contracts for 2027 continue to trade well above pre-conflict averages, suggesting investors expect oil to stabilise at structurally higher levels rather than revisit the $60-per-barrel environment seen before the crisis.

The bottom line

The US–Iran memorandum has significantly reduced fears of an immediate disruption to global energy supplies and reopened the prospect of millions of barrels returning to international markets.

Yet the agreement remains a diplomatic roadmap rather than a final peace settlement.

Much will depend on whether negotiations succeed, sanctions are permanently lifted, and maritime security in the Strait of Hormuz proves durable.

{kind=link}